401(k): 7 Mistakes of Average American’s Life

There are some common mistakes that all investors tend to make with respect to their 401k plans. Here, we will highlight seven of the most common mistakes that an average American may make when investing in their retirement plans.

Mistake #1: Too little

One mistake that a lot of people make is that they don’t save enough. If you want to accumulate $1 million, you must save at least $1,000 per month for 30 years, provided you are earning an annual return of 6%. Not everybody does the math before they start saving. Make sure you increase the amount you set aside for your retirement whenever your income goes up.

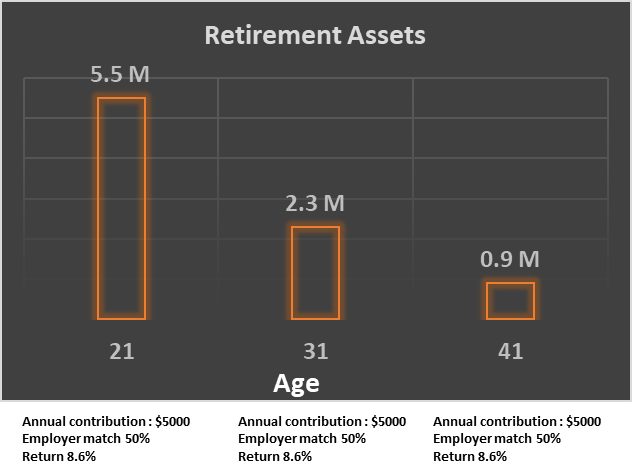

Mistake #2: Too late

Another mistake is to not start saving for retirement early enough. In the financial world, time and compounding interest will always be your allies. The longer the time horizon during which you save, the more the interest will compound for a larger retirement pot. If you start saving right after college, even if it is a small sum, you will certainly have a head start. Once you get habituated to saving, it does get easier. Follow the 2:1 principle: for every 2 years spent working, you have to save for 1 year of retirement. If you delay kicking off the retirement planning process by 10 years and start saving at the age of 31 years, you can only accumulate $2.3 million. Sounds like lot less cash, right? I hear you. If you want to come anywhere close to $5.5 million at this point, you have to contribute 2.5 times i.e. $12,500 a year to get to $5.5 million for retirement. A huge penalty for a late start!

Mistake #3: Saving just enough to get a match

Some employers offer to match up to a specific percentage of the employee’s contributions to the 401(K). This is quite helpful, but don’t let it stop you. You can certainly invest more than what your employer offers to match. For instance, if your employer offers to contribute 50% of what you put aside and your contribution is 6%, then your total contribution to the 401(K) will be 9%. Well, that is certainly good enough, but don’t let this stop you from increasing the amount you can contribute.

There will be some employers who might not want to make any contributions to your 401(K). Well, if that’s the case, then it doesn’t mean that you don’t invest in 401(K) at all. The 401(K) is a great way to make contributions to your retirement fund directly (without seeing the money in your bank account!) So, make the most of this convenient way of saving.

Mistake #4: Investing only in Target Date Funds

Target date funds or TDFs is one set of options for investment in your 401(K). These funds usually have a year present next to the name – the year in which you expect to retire. The idea is that you opt for a TDF that targets the year in around which you would like to retire, invest in it and watch how it works for you. It does sound convenient – doesn’t it? However, when it comes to TDF, there are two things you must always consider. The first is that the fees payable on TDF are on top of underline mutual funds, and secondly, your choice is limited to one family of funds. If it’s a Fidelity TDF, all mutual funds such as US Large Cap, Mid Cap, and International Funds are managed by Fidelity. These mutual funds may not be the best performing funds in their respective category. Before you invest in your 401(K), ensure that you do all your homework and figure out the different investment options available to you.

Mistake #5: Shying away from professional help

You can always ask your colleagues and friends for advice about invest in your 401(K). However, it is a good idea to consult an expert or professional. There are a lot of tools out and apps like Plootus can provide invaluable advice and make financial planning simpler. Don’t shy away from using these apps.

Mistake #6: Not reviewing the plan

The 401(K) plan ensures that money is being contributed directly to your retirement account as soon as you receive your paycheck. It is automated as it relates to depositing the funds, but it calls for a periodic review by you to ensure the funds are optimally invested. A regular review will help you diversify your portfolio, look into other options available and maybe even alter your contribution from time to time if required.

Mistake #7: Borrowing from 401 (k) plan

It is never a good idea to borrow from your 401(K). The two reasons why this isn’t recommended are:

- The money that you don’t invest is the money you aren’t earning. So, if you withdraw money from your 401(K), you are defeating the purpose of saving in it in the first place.

- Borrowing from your 401(K) might attract additional penalties as well as taxes. If you don’t have sufficient funds to repay the loan in time, then you might be looking at a penalty of more than 10%.

Avoiding the enlisted mistakes will have a long-term effect on your returns. It can make all the difference between retiring comfortably and relying on public welfare programs like Social Security that are steadily shrinking.

Luckily, technology has come to our rescue and an app like Plootus has made retirement planning very easy, even for those who are not financially savvy. It is available literally at your fingertips for downloading from the Apple and Android app stores and tells you how much to save and where to invest for a happily ever after. So the next time you pick up your phone to look at Facebook News Feed updates, it may be worth your time to download at Plootus, a ‘financial advisor’ at your disposal. The app will assist you with planning your retirement without having to sacrifice your weekends and weeknights today for a secure tomorrow. I will cover how to choose investments for your retirement planning in my next blog update. Don’t worry if you are not a finance professional or have not done that before! We will take baby steps.

Until next time!

Author: Sunil Gangwani, Co-Founder, Plootus

https://www.Plootus.com:

Download on Apple Store: Plootus |Download on Android Store: Plootus