Pulling the plugs on your retirement plan schemes? Ever a good choice?

Life expectancy is defined as the age to which a person will live. The average lifespan of an American has increased around 15% in the last 70 years. This means that people are living longer. But the only challenge here is the longer you live, bigger are the chances of you running out of your retirement savings.

The future of Social Security looks grim and reports suggest that all the funds will be depleted completely by 2035. This has left most wondering what would happen to their money if Social Security runs out of resources. The Social Security would not completely be out but would be able to honor only 76% of every scheduled payment.

Adding to all this is the fact that one is not allowed to keep money in the retirement schemes indefinitely. You are mandated to take out funds above a certain level as scheduled to keep the penalties away.

Looking at the current trends even the millennials are delaying saving funds in retirement schemes. Most do not have access to employer sponsored schemes and others are reeling under the pressure to repay student loans. Here, they should understand that contributing even a little sum is better than nothing because the annual contribution will only rise as the age of the person increases.

To answer the question whether we should ever stop saving in retirement plan schemes, it is a simple NO. This is because how much ever you save once you retire it is never enough. On the contrary, a person should start as early as possible (refer #2) and get maximum benefits out of the retirement schemes.

Like Ron, if he starts saving at the age of 25 having a growth portfolio he would be in a better position by the time he retires at the age of 65.

Following are 3 scenarios where Ron starts saving at the ages of 25, 35 and 40 and he plans to have $ 1M in his retirement savings by his retirement.

Lets see how different his situations will be in all the 3 scenarios.

Fig1. 1st Scenario – Starting at the age of 25 with the annual contribution of $ 3.1 K

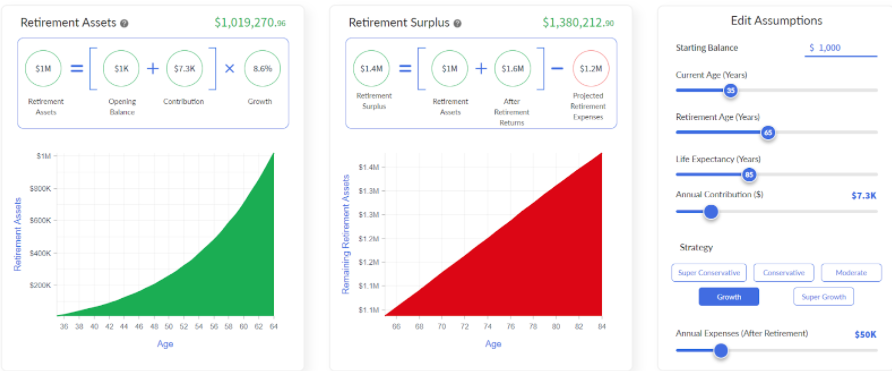

Fig2. 2nd Scenario – Starting at the age of 35 with the annual contribution of $7.3 K

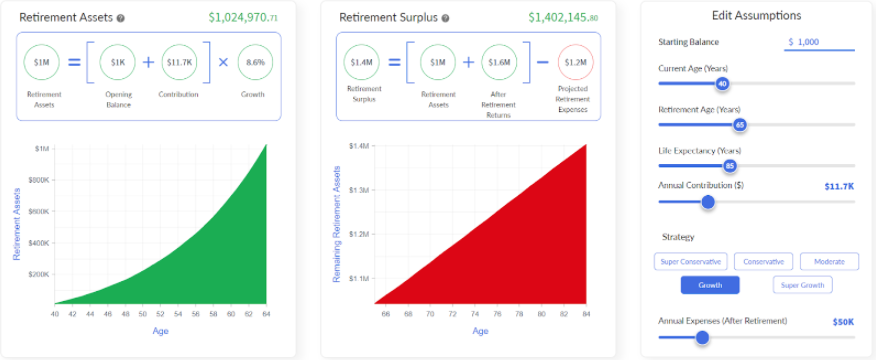

Fig3. 3rd Scenario – Starting at the age of 40 with the annual contribution of $11.7 K

In the meagre duration of 15 years the annual contribution increased around 277%. This emphasizes how important it is to start early and not stop until you retire.

The 401k calculator at Plootus helps you determine how much to invest in your retirement funds on an annual basis to achieve your goal of the amount you wish to have when you retire. This calculator takes into account you current age, annual expenses and also the portfolio strategy you want to maintain to calculate how much lump sum amount will be accumulated in your account by the time you retire. This calculator works on an algorithm and makes best recommendations to you.

The phrase “make your money work” holds true in retirement savings and it’s up to you how much benefits you take out of it. Hence, you should never stop investing in your retirement funds and rather start as early as possible to make the most out of it.

Until next time!

Be Safe & Healthy,

Sunil Gangwani

Sneha Kotian

Download on Apple Store: Plootus

Download on Android Store: Plootus