Save on Hidden Fees

Plootus optimizes your 401k, 403b, 457 or TSP retirement account. Budget smarter, and Manage all your Financial Accounts in One Place.

More ways to cut costs and grow your wealth!

Plootus collaborates with select platforms to help you compare, save, and manage your money more efficiently.

Disclaimer: Plootus (an SEC-registered investment advisor) may receive compensation for referrals to third-party products and services, listed on our Partners page. These referrals are for informational purposes only and do not constitute an endorsement or recommendation. Plootus has not conducted due diligence on, nor assumes responsibility for, any third-party offerings. Users are encouraged to evaluate these options independently before making any decisions.

What Plootus does — Better than anyone else!

Everything You Need to Take Control of Your Finances

From tracking your accounts to budgeting and personalized investment advice, Plootus simplifies your financial life and helps you plan for the future.

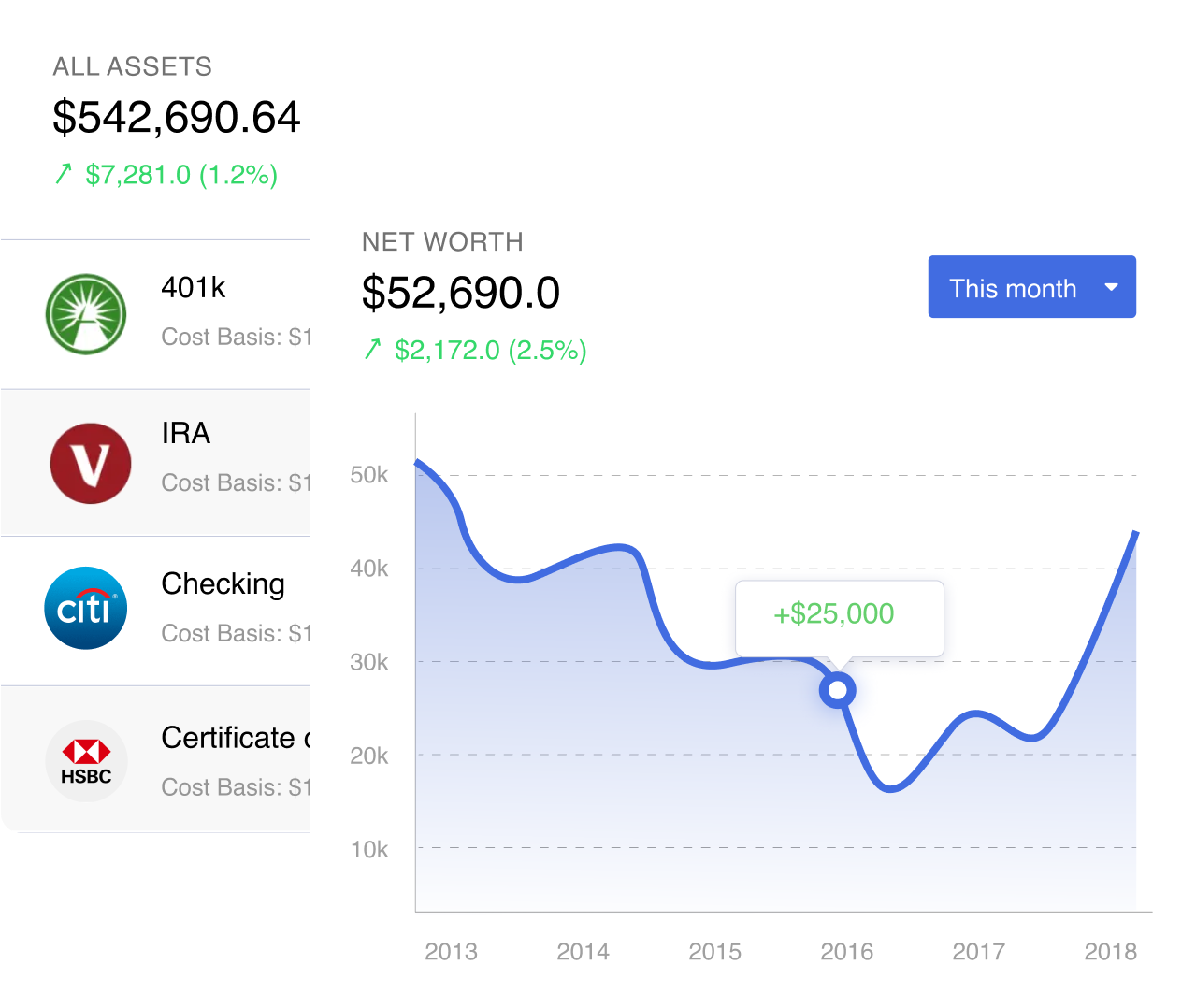

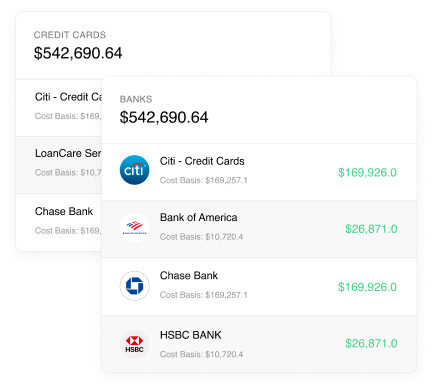

Track All Your Financial Accounts

Effortlessly manage all your finances in one place. Plootus links your accounts, giving you real-time updates on your checking, savings, credit card and investment account balances so you can stay on top of your financial health.

Seamless Account Integration

Ability to link 14,000+ checking, savings, credit card, & investment accounts for a complete view of your finances. Plootus allows you to view all your finances in one place, providing real-time insights to help you manage and grow your wealth.

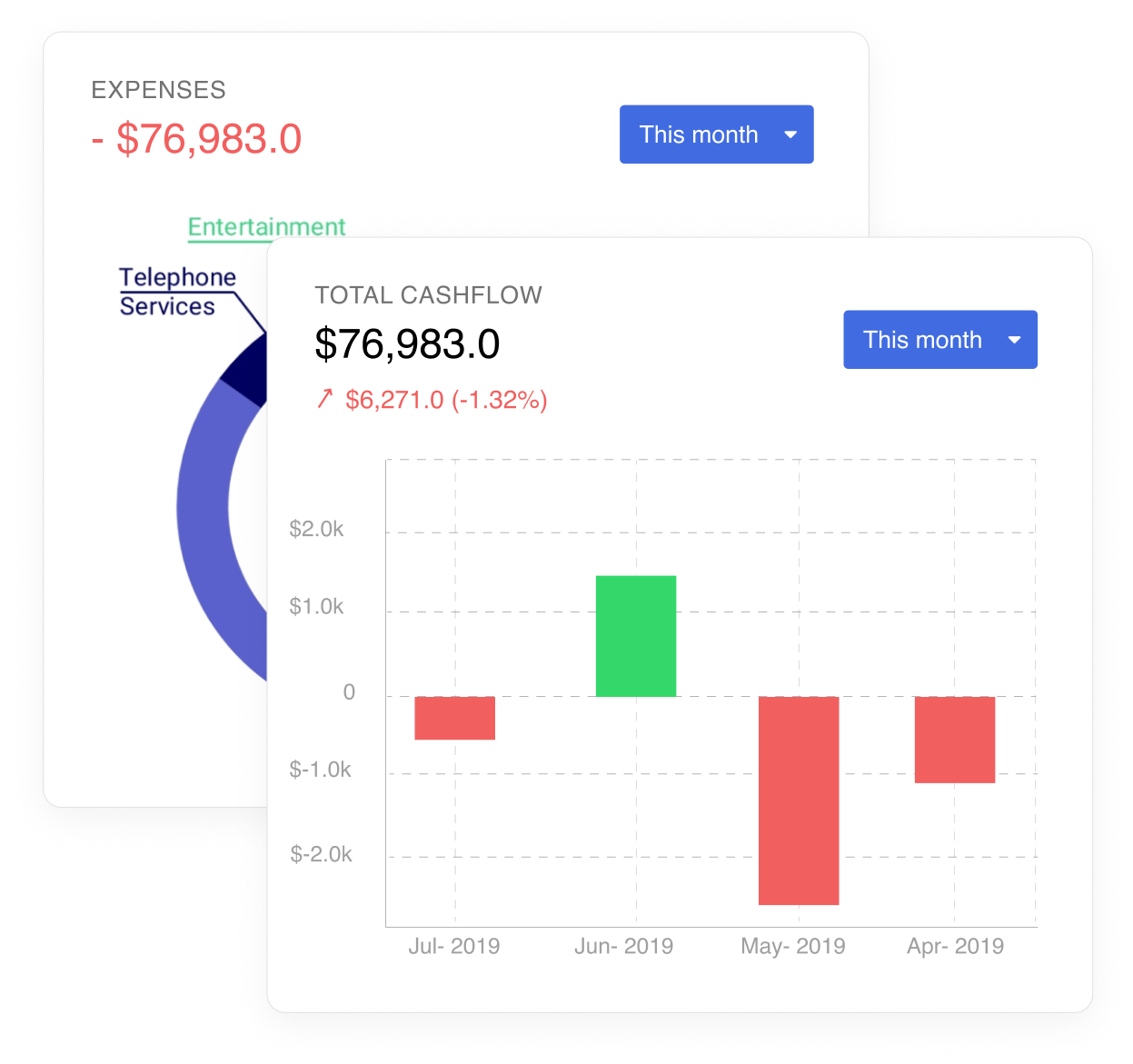

Expense And Savings Analysis

Understand exactly where your money is going. Plootus breaks down your expenses and savings with detailed insights, helping you budget more effectively and find areas to save.

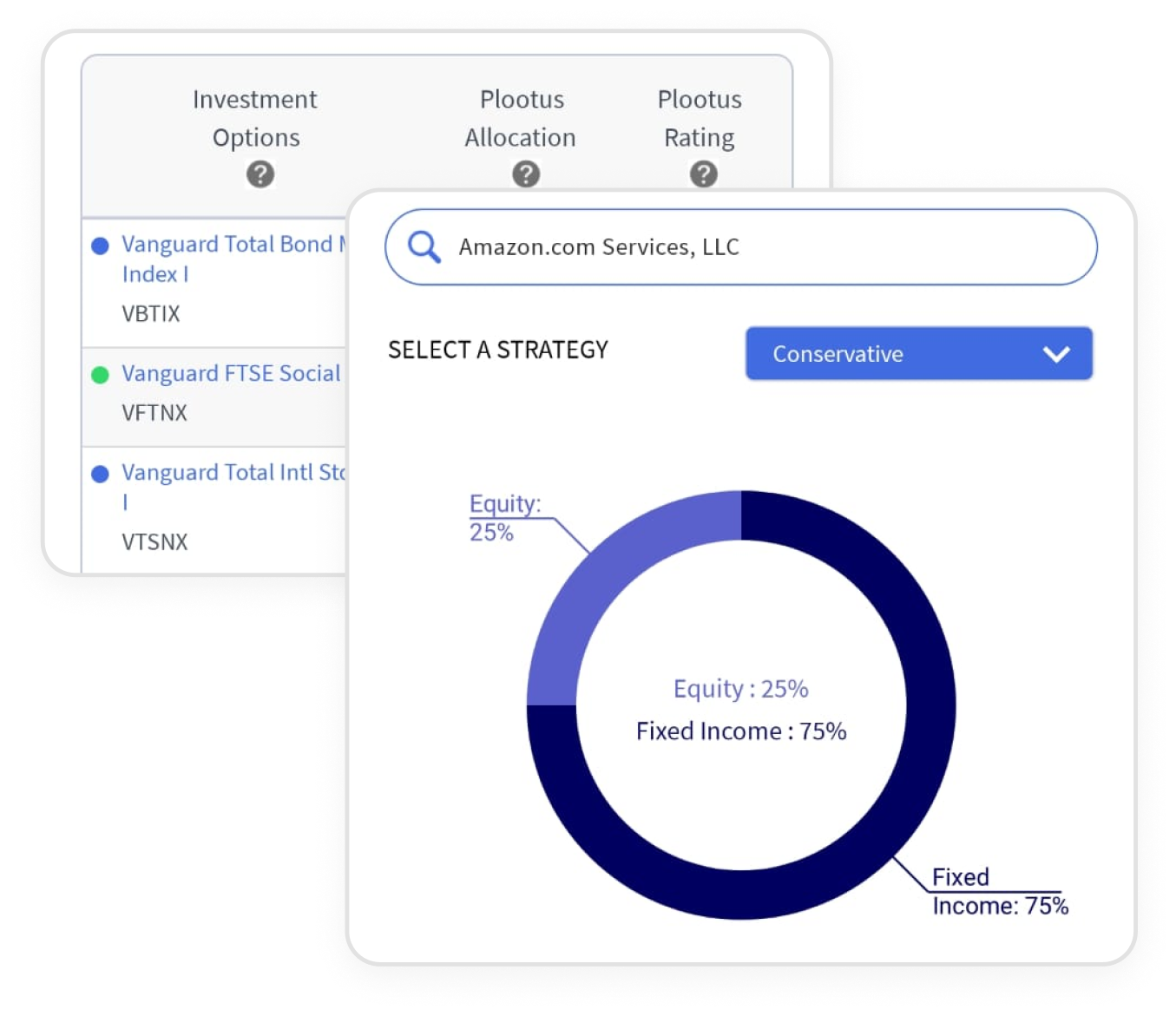

Investment And Retirement Advice

Beyond tracking, we offer smart advice for growing your 401k/403b and other retirement accounts. Plootus offers personalized advice to optimize your portfolio, reduce fees, and ensure you're on track to meet your financial goals.

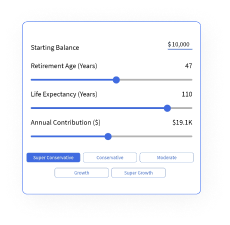

Calculate your savings journey with our

AI-enabled Retirement Calculator

Plootus removes the guesswork from retirement planning. Our AI analyzes your financial landscape and regional spending patterns— based on your zip code—to project how much you'll need for retirement.

Adjust your risk strategy and contributions to stay on track and confidently achieve your goals.

TRY IT NOW

Plootus In The News

What Our Users Say!

Read Our Blogs